Cooling Industrial Market Signals a Return to Normal

March 7, 2024

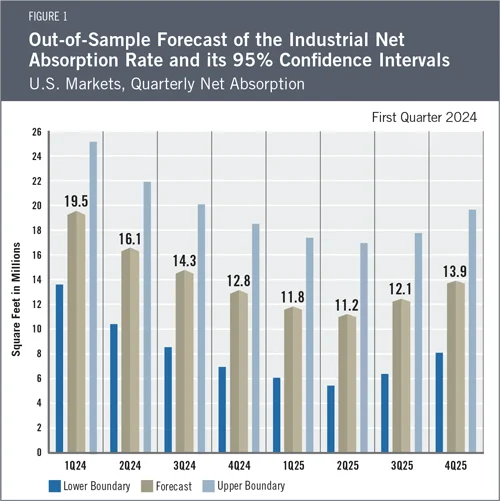

The NAIOP Research Foundation has published the NAIOP Industrial Space Demand Forecast for Q1 2024.

The NAIOP Research Foundation has published the NAIOP Industrial Space Demand Forecast for Q1 2024.

Key takeaways:

- The national office market experienced total negative net absorption of 21.3 million square feet through the fourth quarter of 2022 and the first quarter of 2023, bringing the vacancy rate to 17.8 percent, the highest level since the second quarter of 1993.

- The COVID-19 public health emergency officially ended in the United States on May 11, 2023, but remote and hybrid work arrangements remain largely in place and continue to negatively affect demand for office space.

- A currently strong labor market is combining with fears of a looming recession to limit occupiers’ interest in signing new leases. With the unemployment rate at 3.4 percent, the lowest since 1969, the competition for talent is supporting the continuation of hybrid and remote work policies.

- Few firms are interested in expanding the amount of space they lease as they prepare for a potential recession later this year. As a result, while office-using employment has risen to 5.4 percent above pre-pandemic levels, occupied office space is 3.5 percent below pre-pandemic levels, and the average amount of office space per employee has fallen to a 22-year low of 152 square feet. Given these trends, net office space absorption in the remaining three quarters of 2023 is expected to be negative 24.4 million square feet. Moving forward, the forecast projects that net absorption will turn positive in 2024 and will total approximately 30.6 million square feet for the year.

Read more »